Britain still produces some of the world’s best engineering firms, such Avingtrans - which sells & services (ie 36% aftermarket) mission-critical components to the rapidly expanding new nuclear (eg Terrapower), existing nuclear (life extension & decommissioning), defence, energy, datacentre/AI and healthcare sectors.

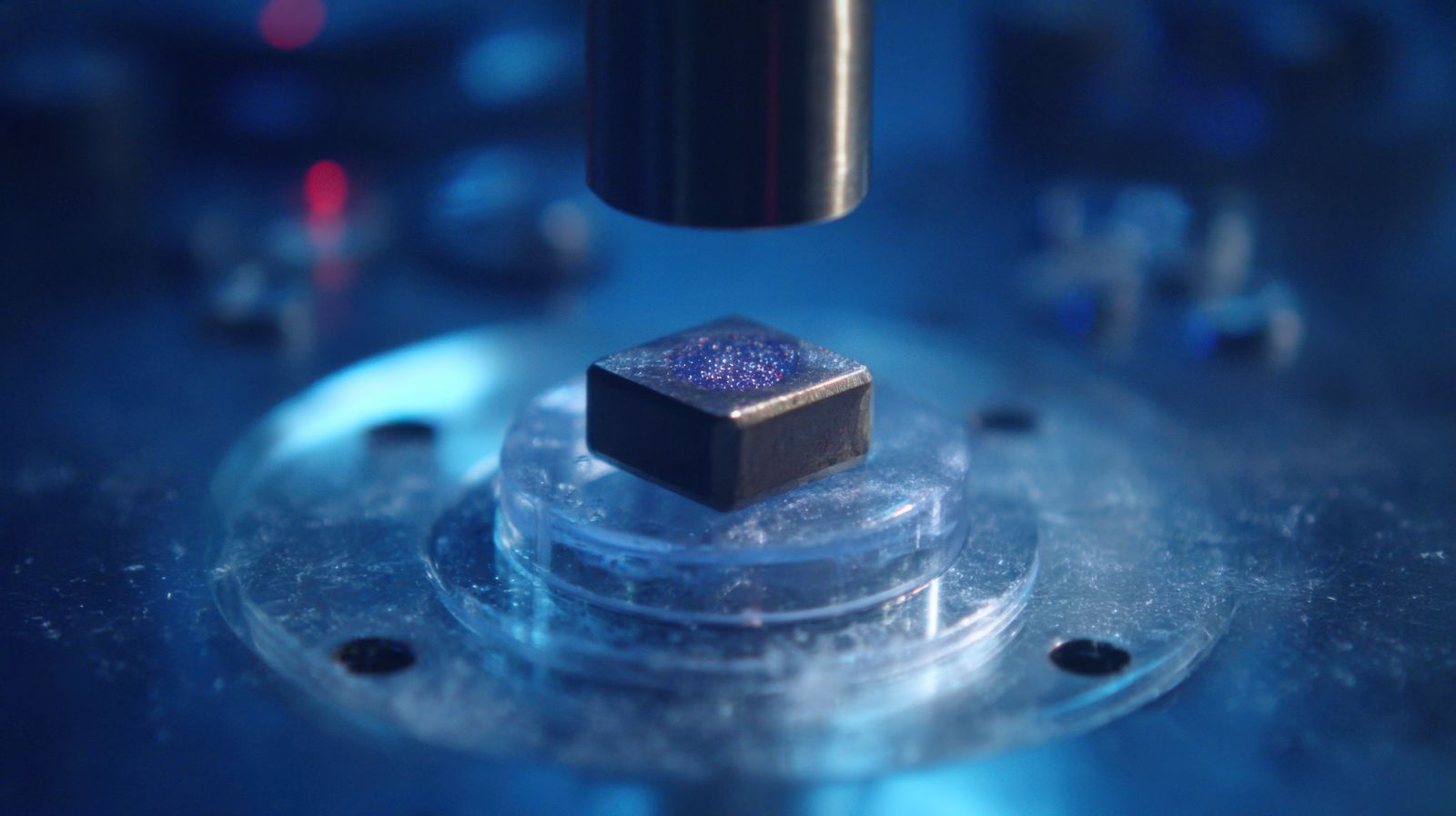

But that’s not all. This morning the company said that its Scientific Magnetics (SciMag) subsidiary had achieved a major milestone in shipping its 20th superconducting magnet for quantum computing applications. These machines, albeit not yet commercially available, can process data 100s of times (if not 1,000s) faster than the best CPUs or GPUs on the market.

Here SciMag manufactures tailored WET and DRY (Cryogen Free) superconducting magnet solutions and has over 30 years' expertise in qubit noise performance/reduction. Positioning the business as key partner for qubit magnet technologies and quantum computing more generally.

Better still last week Rt Hon Rachel Reeves announced plans to make the UK the first country in the world to roll out quantum computers at scale. Additionally promising £2.5 billion of investment with the intention of helping to create >100,000 jobs over the next two decades, alongside adding £212 billion to GDP.

Several leading technology companies, research institutions and startups already possess operational quantum computers, with commercial-scale systems expected to require multiple precision magnet systems per installation. As well as quantum computing, SciMag also makes advanced superconducting and resistive magnet systems for customers in MRI, scientific research and medical physics.

Clint Gouveia, MD of Scientific Magnetics, commenting: "Delivering our 20th superconducting magnet for quantum computing applications is a significant achievement for our team, who are working at the leading edge of the quantum computing revolution. With a further 18 systems in production and a strong forward order book, we are developing a promising position as a key supplier of the precision magnet systems needed to produce future quantum computers at scale."

Wrt the group's May FY’26 numbers, analysts are forecasting £175m of revenue, £20.5m EBITDA and EPS of 30.4p – putting the shares on 18.1x earnings and 9.9x EV/EBITDA. Hence the stock offers investors excellent visibility (95%+ sales cover), multiple secular tailwinds and embedded upside optionality in medical imaging & quantum computing.

Lastly over the next few years, shareholders could also enjoy some hefty capital returns, thanks to possible disposals of Hayward Tyler & Ormandy, alongside a potential IPO of Medical division (including SciMag).